When to Drop Collision Insurance Coverage: Top 5 Smart Reasons 2025

When to Drop Collision Insurance Coverage

Wondering when to drop collision insurance coverage? Here’s a quick guide to help you decide:

You should consider dropping collision insurance coverage if:

– Your car is older or worth less than $5,000.

– Your annual collision premium exceeds 10% of your vehicle’s market value.

– You’re comfortable paying out-of-pocket for repairs or replacement.

– You no longer have a loan or lease obligation requiring collision coverage.

Collision coverage can provide peace of mind, but there comes a time when the cost outweighs the benefit of protection. We’ll clarify exactly when and why you might consider cancelling collision insurance, giving you confidence in your decision and helping you save money.

I’m Geoff Stanton, a Certified Insurance Counselor (CIC) and the President at Stanton Insurance in Waltham, Massachusetts. With over two decades of experience in claims and risk management, I regularly advise individuals and families on important insurance decisions, including when to drop collision insurance coverage.

When to drop collision insurance coverage helpful reading:

– do you need collision coverage

– collision vs comprehensive

– what is collision insurance

Deciding when to drop collision insurance coverage involves a careful analysis of your financial situation, your vehicle’s current value, and your risk tolerance. Let’s break down the key factors that should influence your decision.

The Annual Premium Factor

One of the most important considerations is how much you’re paying for collision coverage annually. Insurance is ultimately a financial product, and like any financial decision, it should make economic sense for your situation.

At Stanton Insurance Agency, we recommend that clients closely examine their premium costs in relation to potential benefits. If you’re paying $600 annually for collision coverage on a vehicle that’s rapidly depreciating, those dollars might be better allocated elsewhere in your financial plan.

Your Vehicle’s Value

The current market value of your car is perhaps the most critical factor in determining when to drop collision insurance coverage. As vehicles age, they naturally depreciate, making the potential insurance payout in case of an accident progressively smaller.

To determine your car’s current value, you can use resources like:

– Kelley Blue Book

– NADA Guides

– Edmunds

– Recent comparable sales in your area

Insurance companies will pay the actual cash value (ACV) of your vehicle at the time of the loss, not what you paid for it or what it would cost to replace it with a new model.

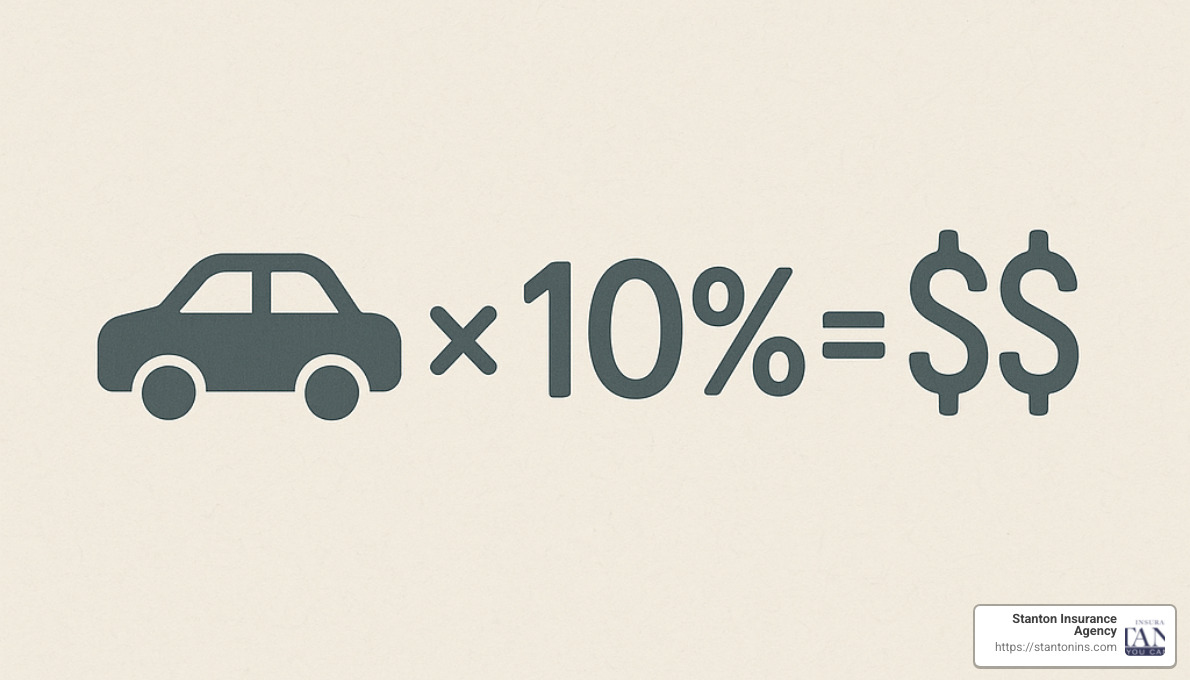

The 10% Rule: A Practical Guideline

At Stanton Insurance Agency, we often recommend the “10% rule” as a practical guideline for clients wondering when to drop collision insurance coverage. This rule suggests that if your annual collision premium costs more than 10% of your car’s value, it may be time to drop the coverage.

For example:

– If your car is worth $4,000

– And your annual collision premium is $450

– That’s more than 10% of your car’s value ($400)

– This suggests it might be time to consider dropping collision coverage

This rule isn’t absolute, but it provides a useful benchmark for making an informed decision about your coverage needs.

Factors to Consider Before Dropping Collision Coverage

Deciding when to drop collision insurance coverage depends on more than just numbers. To make the best choice, it’s important to evaluate your car’s age, value, your personal comfort with risk, and any financial obligations you may still have on your vehicle.

Car Age and Depreciation Curve

Understanding how your vehicle loses value (depreciates) over time will help you make a smarter insurance decision. When cars are brand new, they lose a lot of value quickly—typically about 20-30% in the first year alone. In the second year, vehicles generally depreciate about 15-20%, then another 10-15% in their third year. After that, depreciation usually slows down to a steadier 7-12% each year.

So, if your car has already weathered those first few steep drops in value and settled into a gentler depreciation pace, deciding when to drop collision insurance coverage becomes clearer. At this point, you’re likely insuring a vehicle that won’t yield a significant payout if damaged. It may no longer make sense to pay a premium that’s close to—or even higher than—the vehicle’s worth.

Your Personal Risk Tolerance

Aside from the cold hard facts and numbers, your comfort level with risk is a crucial factor. Imagine you chose to drop collision coverage and, unfortunately, your car got damaged or totaled in an accident. Would you comfortably manage paying out-of-pocket to either repair or replace your vehicle? Consider how losing your car—even temporarily—could impact your day-to-day responsibilities and routine.

At Stanton Insurance Agency, we’ve noticed that our clients all approach risk differently. Some drivers prefer the security blanket of knowing they’re covered no matter what, while others feel more comfortable saving on premiums and handling minor repairs themselves. Ask yourself honestly how you’d handle unforeseen auto repair costs, and factor that into your decision about when to drop collision insurance coverage.

Also, don’t forget to think about your backup transportation options. If you live somewhere with great public transit or have another vehicle available, you’re probably in a better position to drop collision coverage compared to someone relying solely on one vehicle in a rural area.

Loan and Lease Requirements

One crucial factor that’s often overlooked is your financial obligation to your lender or leasing company. If you’re still repaying a car loan or leasing your vehicle, the decision about your collision coverage might already be made for you. Virtually all lenders and leasing companies require you to maintain full coverage—including collision insurance—until you’ve fully paid off your loan or your lease agreement comes to an end.

So, before deciding when to drop collision insurance coverage, double-check your finance documents or lease agreement carefully. Ensure you understand exactly what’s required, because dropping coverage too soon could lead to unwanted headaches down the road.

Once your loan or lease obligation is complete, you’ll have greater freedom and flexibility to make a decision based solely on your personal financial situation, your vehicle’s value, and your comfort with risk.

For additional help, these resources on our site can guide you further:

– do you need collision coverage

– collision vs comprehensive

– what is collision insurance

The decision about dropping collision coverage is personal and involves thinking carefully about these factors. Evaluating your car’s depreciation, your comfort level with financial risk, and any lingering loan or lease obligations ensures you choose the coverage that’s right for you.

Scenarios When Dropping Collision Coverage Makes Sense

Deciding when to drop collision insurance coverage is all about finding the right balance between cost and protection. While everyone’s situation is unique, there are some common scenarios where reducing or canceling collision coverage can make a lot of financial sense.

When You Rarely Use Your Vehicle

If your car spends more time parked in the driveway or garage than on the open road, the chances of a collision are naturally lower. Maybe you’re commuting primarily by public transportation, or perhaps you own a second car that rarely sees action. In these situations, paying for collision coverage might not provide good value for your money.

At Stanton Insurance Agency, we’ve helped plenty of clients in the Boston area who rely on the T or other public transit options. For these folks, collision insurance on an infrequently driven vehicle often just doesn’t make sense.

When Your Car’s Value Has Significantly Declined

Your car’s market value is a key factor in determining when to drop collision insurance coverage. Generally speaking, if your vehicle is worth less than $3,000 to $5,000, the payout you’d receive after an accident might not justify the cost of the coverage.

Let’s say your car is valued at around $3,500, and your collision deductible is $1,000. In a worst-case scenario—like a total loss—you’d only receive $2,500. If you’re paying hundreds of dollars each year in collision premiums, you might decide it’s smarter to save that money instead.

When Insurance Premiums Are Disproportionately High

Sometimes, even older cars can carry surprisingly high collision premiums. This can happen for various reasons—like high repair costs, scarce replacement parts, a history of frequent claims on the model, or even your own driving record.

If you’re noticing your premiums climbing despite your vehicle’s decreasing value, that’s a clear indicator it may be time to drop collision coverage. You’d be paying a lot for relatively little protection.

When You Can Comfortably Cover Out-of-Pocket Repair Costs

Insurance exists to protect you from financial hardships you couldn’t easily manage on your own. But what if you have a comfortable emergency fund or solid savings set aside for unexpected expenses? In that case, you might feel confident skipping collision coverage altogether and “self-insuring.”

Plenty of our customers at Stanton Insurance Agency choose this path for older cars. If you’re financially comfortable covering repairs or even purchasing a replacement vehicle without stress, collision insurance might be a cost you can safely drop.

When Repair Costs Regularly Exceed Your Deductible

Another scenario worth considering is if most of your car’s typical repairs cost less than—or close to—your deductible. Imagine your deductible is $1,000, but your car’s common repairs, like fixing minor damage or replacing a bumper, usually run around $800-$900. Since you’d be paying these costs out-of-pocket anyway, collision coverage may not offer much practical value.

When You’d Prefer to Replace Rather Than Repair

Lastly, consider your personal preference if your car experiences major damage. Some drivers we work with have already decided they’d rather replace their aging vehicle than shell out money for repairs. If that’s your mindset, collision insurance might not align with your plans—and dropping it could be a wise financial choice.

The decision about when to drop collision insurance coverage depends on your unique circumstances, personal finances, and risk comfort level. By thoughtfully considering these scenarios—and perhaps consulting with trusted experts at Stanton Insurance Agency—you can confidently make the choice that best suits your life and wallet.

Steps to Take After Deciding to Drop Collision Coverage

So you’ve weighed the numbers, considered your vehicle’s value, and finally decided when to drop collision insurance coverage. Congratulations on making this informed decision! But your journey isn’t quite over yet—there are still a few essential steps to ensure you transition smoothly.

Consult with Your Insurance Agent

First things first: talk it over with your trustworthy insurance agent at Stanton Insurance Agency (that’s us!). Dropping collision coverage isn’t a one-size-fits-all decision, and it’s crucial to make sure you haven’t inadvertently opened yourself up to coverage gaps.

When we sit down together, we’ll take a good look at your entire insurance portfolio—auto, home, personal, business—to make sure everything aligns neatly. We’ll identify potential risks, suggest other protective measures if needed, and double-check that dropping collision coverage genuinely makes sense for you. Our team serves Massachusetts, New Hampshire, and Maine and knows how local factors can impact your insurance needs.

Review Your Policy Details Carefully

Next up, it’s time to read the fine print (preferably with a cup of coffee in hand!). Carefully review your insurance policy to fully understand what happens when you remove collision coverage. You want to be clear on:

- Exactly when your collision coverage will end

- How removing this coverage will change your overall insurance premium (hopefully saving you money!)

- Which coverages remain active and will still offer protection

- Any discounts that might disappear once you drop this coverage

At Stanton Insurance Agency, we’ll walk you through these details step by step, so you’re never left guessing.

Consider a Gradual Coverage Reduction

If you’re feeling a bit hesitant about dropping collision coverage completely, that’s completely understandable. A gradual approach could be perfect for you. Start by increasing your collision deductible, which lowers your premium without fully removing your coverage. This way, you still have a safety net—just a slightly smaller one!

After about 6-12 months, revisit the decision. As your car continues to age and its value declines further, reassess if the time is right to completely drop collision coverage. Eventually, there will be a natural point when the coverage just doesn’t add enough value anymore.

This gradual transition can help you ease into the idea of being completely self-insured for collision damages, making the decision feel comfortable and stress-free.

There’s no rush. Every insurance decision should feel right for your wallet and your peace of mind. At Stanton Insurance Agency, our goal is always to help you confidently steer these important choices, ensuring your valuable assets remain protected without breaking the bank.

Frequently Asked Questions about Dropping Collision Insurance Coverage

Let’s tackle some of the most common questions we hear from drivers considering whether to drop their collision coverage. These questions might be on your mind too as you weigh this important insurance decision.

At what value should you drop collision coverage?

If you’re wondering about the right time to drop collision coverage, most insurance professionals (myself included) point to the $3,000-$5,000 vehicle value range as the typical “sweet spot.” When your car’s value drops below this threshold, the math often stops making sense.

10% rule we talked about earlier? It’s worth repeating because it’s so practical. If your annual collision premium costs more than 10% of what your vehicle is actually worth, you’re probably at the point where dropping this coverage makes financial sense.

For example, paying $450 a year to protect a car worth $4,000 (that’s 11.25% of the car’s value) suggests it might be time to reconsider your coverage. After all, insurance should protect you from financial hardship, not create it through unnecessarily high premiums!

Every situation is unique, though. If you’re in Massachusetts, New Hampshire, or Maine and want personalized guidance based on your specific vehicle and circumstances, we’re always happy to provide a custom assessment at Stanton Insurance Agency.

Is collision worth it on an older car?

The value of collision coverage on older vehicles diminishes pretty quickly as several factors converge:

Your car’s actual cash value (ACV) continues its downward march each year. Meanwhile, that gap between your deductible and what your car is worth keeps shrinking. Before long, you might find yourself in a situation where potential repair costs after an accident could approach or even exceed what the entire vehicle is worth.

That said, there are still some situations where keeping collision on an older car makes sense. If your vehicle is a classic with value beyond its market price, if you absolutely depend on this car and couldn’t easily replace it, or if you regularly drive in particularly hazardous conditions, the coverage might still be worth it.

I had a client last year with a 12-year-old sedan worth about $3,500. She lived on a rural road with frequent deer crossings and had already experienced two collisions in the past three years. For her specific situation, keeping collision coverage made sense despite the car’s age and value.

At Stanton Insurance Agency, we believe in looking at your complete picture rather than making decisions based solely on your car’s age or some arbitrary rule.

When does collision insurance stop being beneficial?

There are several clear signals that collision coverage may no longer be providing good value for your insurance dollar:

When your deductible represents a significant chunk of your car’s value, the math changes dramatically. A $1,000 deductible on a $4,000 car means you’d only receive $3,000 at most after an accident—and that’s assuming a total loss. For smaller accidents, you might not even meet the deductible threshold.

Collision insurance typically stops being beneficial when your annual premium costs more than the protection value it provides. This is essentially a risk/reward calculation—if you’re paying $500 annually to protect a potential $2,500 payout (after deductible), you’d break even after just five years without an accident.

The coverage also becomes less valuable when you have enough savings to comfortably self-insure. If replacing your vehicle wouldn’t create financial hardship, you might be better off putting those premium dollars toward other priorities.

Finally, when your vehicle has depreciated to the point where even moderate damage would likely result in the insurance company declaring it a total loss, collision coverage provides diminishing returns. According to the Insurance Information Institute, understanding when to adjust your coverage is an important part of managing your overall insurance costs.

While dropping collision coverage can certainly save you money on premiums, it’s important to recognize what you’re doing: you’re transferring the financial risk of accidents entirely to yourself. This is why the decision shouldn’t be made lightly or based solely on your car’s age or value.

I always recommend a comprehensive assessment that takes into account your complete financial situation, the true value of your vehicle, and your personal comfort with risk. After all, insurance is ultimately about helping you sleep better at night—and that peace of mind looks different for everyone.

Conclusion

Deciding when to drop collision insurance coverage isn’t always easy—it’s a personal choice that requires balancing your financial situation with your comfort level for risk. While guidelines like the 10% rule and the $3,000-$5,000 vehicle value threshold offer helpful starting points, the right decision ultimately depends on your unique circumstances, priorities, and financial goals.

At Stanton Insurance Agency, we believe the best insurance choices happen when you’re informed and confident. Our goal is to serve as your trusted advisor, helping you steer these important decisions as your life and vehicle ownership journey evolves. Whether you live in Massachusetts, New Hampshire, or Maine, our experienced team is committed to guiding you through every stage, from buying your first car to deciding when collision insurance no longer makes sense.

The key takeaway is understanding the trade-offs clearly. Dropping collision coverage can save you money on premiums—but it means taking on the full financial responsibility if your vehicle is damaged or totaled. If you’ve carefully considered your car’s value, your annual premiums, potential repair costs, and your own resources and risk tolerance, you can feel confident making the decision that’s right for you.

If you’re still unsure or just want a friendly second opinion, don’t hesitate to reach out to us at Stanton Insurance Agency. Our team is always here to chat, answer your questions, and help you steer toward decisions you’ll feel good about.