Apartment Owner Insurance: 5 Best Ranked Providers 2024

Why Apartment Owner Insurance is Critical for Your Investment

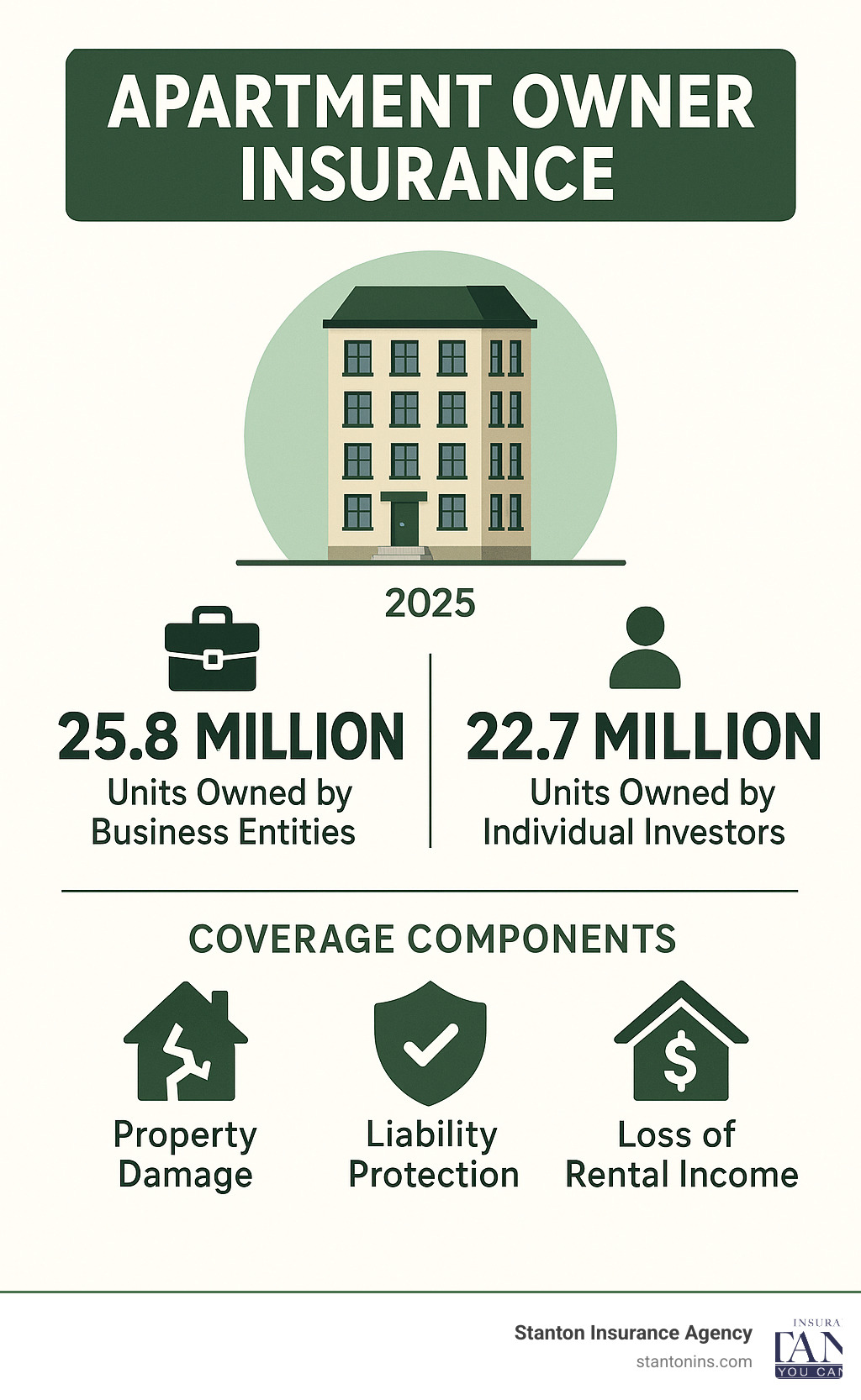

Apartment owner insurance protects property owners from the unique risks of renting residential units to tenants. Unlike standard homeowner’s insurance, this specialized coverage addresses liability claims, property damage, and lost rental income specific to multi-unit properties.

Quick Answer – What You Need to Know:

- Coverage Types: Property damage, general liability, loss of rental income, equipment breakdown

- Who Needs It: Owners of single units, multi-unit buildings, mixed-use properties, vacation rentals

- Average Cost: $67-$89/month for $1M/$2M general liability; property coverage varies by building value

- Key Difference: Covers non-owner occupied properties and rental income protection

- Legal Requirement: Not mandatory but highly recommended for financial protection

The apartment rental market faces mounting pressures. Research shows that over 40% of U.S. renter households experienced rental shortfalls during the Covid-19 crisis, putting nearly 12 million families at risk of eviction. Meanwhile, 35% of American renters have little to no confidence in their ability to make next month’s rent.

These economic strains create cascading risks for property owners. Tenant-related claims, property damage, and lost rental income can devastate an investment without proper coverage. Standard homeowner’s policies won’t protect rental properties, leaving owners exposed to lawsuits, repair costs, and vacancy losses.

Business entities like LLCs and partnerships own 25.8 million apartment units nationwide, while individual investors control another 22.7 million units across 16.7 million properties. Each faces distinct insurance challenges based on property type, location, and tenant demographics.

I’m Geoff Stanton, President of Stanton Insurance Agency and a 4th generation owner with over 25 years in the industry. I specialize in commercial property and liability coverage, helping apartment owners steer complex apartment owner insurance decisions to protect their rental investments.

Apartment owner insurance terms to learn:

How We Ranked the Best Apartment Owner Insurance Providers

Our ranking methodology evaluates providers across multiple dimensions critical to apartment owners’ success. We analyzed financial strength ratings, coverage breadth, claims service quality, premium flexibility, and specialized features unique to rental property insurance.

Financial Strength: We prioritized carriers with A.M. Best ratings of A- or higher, ensuring they can pay claims during catastrophic events. Financial stability becomes crucial when facing large liability settlements or widespread property damage.

Coverage Breadth: Top providers offer comprehensive protection including dwelling coverage, general liability, loss of rental income, equipment breakdown, and ordinance & law endorsements. We evaluated optional add-ons like cyber liability, tenant discrimination defense, and non-payment of rent coverage.

Claims Service: Response time, adjuster expertise, and settlement practices directly impact your recovery after a loss. We assessed 24/7 claim reporting, dedicated commercial adjusters, and business interruption specialists.

Premium Flexibility: Cost-effective options matter for cash flow management. We examined deductible choices, multi-property discounts, bundling opportunities, and payment plan flexibility.

Specialized Features: Apartment owners face unique risks requiring custom solutions. We evaluated vacancy endorsements, tenant-caused damage coverage, assault & battery protection, and green upgrade benefits.

Scoring Criteria at a Glance

Our weighted scoring system emphasizes factors most critical to apartment owners:

- Financial Strength (25%): A.M. Best ratings, surplus capacity, reinsurance backing

- Coverage Options (20%): Policy forms, endorsements, limits availability

- Claims Service (20%): Response times, adjuster quality, settlement practices

- Premium Competitiveness (15%): Rate adequacy, discount programs, payment flexibility

- Digital Tools (10%): Online portals, mobile apps, certificate generation

- Risk Engineering (10%): Loss control services, safety inspections, mitigation credits

We also considered catastrophe modeling capabilities, coastal appetite, and sustainability initiatives that benefit environmentally conscious property owners.

2024 Provider Categories & Our Rankings

The apartment owner insurance market segments into distinct categories, each serving different property owner needs. National carriers offer broad coverage and bundling opportunities, while specialty underwriters focus exclusively on habitational risks. Regional mutuals provide community-focused service, and digital platforms emphasize convenience and speed.

National Multi-Line Carriers leverage extensive resources and product breadth but may lack specialized apartment expertise. Specialty Habitational MGAs understand rental property risks intimately but often have limited geographic appetite. Regional Mutuals offer personalized service and dividend potential while Independent-Agent Marketplaces provide choice and advocacy. Digital-First Platforms streamline the buying process but may sacrifice coverage customization.

1. National Multi-Line Carriers – Gold Tier

National carriers dominate the apartment insurance landscape through comprehensive coverage packages and substantial financial resources. These providers excel at bundling property, liability, and umbrella coverage while offering multi-state portfolio management for larger investors.

Strengths: Extensive umbrella limits up to $50 million, equipment breakdown coverage, coastal appetite in select markets, and integrated business interruption protection. Many offer green upgrade benefits and ordinance & law coverage as standard features.

Coverage Advantages: Bundled packages combining general liability, commercial property, and business income under unified policy terms. Equipment breakdown coverage protects against HVAC failures, elevator malfunctions, and boiler explosions common in multi-unit buildings.

Target Properties: Multi-state portfolios, newer construction, properties with modern safety systems, and owners seeking comprehensive coverage packages.

Considerations: Premium costs may exceed specialty carriers for older buildings or high-risk locations. Underwriting guidelines can be restrictive for wood-frame construction or properties with previous claims.

2. Specialty Habitational MGAs – Silver Tier

Specialty underwriters focus exclusively on apartment and rental property risks, developing expertise in tenant-related exposures and property-specific challenges. These providers often accept risks that national carriers decline, particularly older construction and challenging locations.

Unique Capabilities: Coverage for wood-frame buildings with sprinkler systems, tenant discrimination defense, vacancy endorsements up to 180 days, and high-limit claims advocacy. Many offer assault & battery coverage for properties in higher-crime areas.

Specialized Endorsements: Tenant legal liability coverage, non-payment of rent insurance, professional liability for property managers, and improved water damage protection including sewer backup and overland flood.

Target Properties: Older buildings, wood-frame construction, properties with challenging tenant demographics, and owners requiring specialized coverage features.

Service Excellence: Dedicated apartment underwriters, property inspection services, and claims adjusters experienced in tenant-related losses. Many provide 24/7 legal helplines for eviction and landlord-tenant disputes.

3. Regional Mutuals & Captives – Bronze Tier

Regional mutual insurance companies emphasize community relationships and policyholder dividends while offering competitive coverage for local apartment owners. These providers often have fewer exclusions and more flexible underwriting guidelines.

Community Focus: Local market knowledge, personalized property inspections, and relationships with regional contractors and restoration vendors. Many offer storm-hardening credits for hurricane shutters, impact windows, and roof upgrades.

Dividend Programs: Mutual structure returns profits to policyholders through dividends, effectively reducing long-term insurance costs. Some mutuals have paid dividends consistently for decades.

Flexible Underwriting: Willingness to consider unique properties, alternative construction materials, and properties with minor maintenance issues. Personal relationships with underwriters facilitate coverage modifications.

Target Properties: Properties in the mutual’s service territory, buildings with good maintenance records, and owners seeking long-term insurance partnerships.

4. Independent-Agent Marketplaces – Value Pick

Independent agents provide access to multiple carriers while offering customized policy design and renewal advocacy. This approach allows apartment owners to optimize coverage while maintaining competitive pricing through market competition.

Carrier Choice: Access to 10-50 insurance companies through a single agent relationship. Agents can layer coverage from multiple carriers or switch carriers at renewal for optimal terms.

Customization: Custom deductible structures, policy limits, and endorsement combinations. Agents can design coverage specific to property type, location, and risk tolerance.

Advocacy Services: Renewal negotiation, claims advocacy, and certificate tracking. Many agents provide risk management consulting and loss control recommendations.

Value Proposition: Competitive pricing through market competition, coverage customization, and ongoing service without carrier loyalty constraints.

5. Digital-First Insurtech Platforms – Up-and-Coming

Digital platforms streamline the apartment insurance buying process through online applications, instant quotes, and mobile policy management. These providers leverage technology to reduce costs while improving customer experience.

Technology Advantages: AI-powered underwriting, instant quote generation, digital policy documents, and mobile claims reporting. Some platforms offer smart device discounts for connected security systems and water leak detectors.

User Experience: Online dashboards for policy management, certificate generation, and claims tracking. Mobile apps provide 24/7 access to policy information and emergency contact numbers.

Efficiency Benefits: Faster policy issuance, automated renewals, and paperless claims processing. Digital platforms often complete the entire insurance transaction online without phone calls or meetings.

Considerations: Limited coverage customization compared to traditional carriers. New companies may lack the claims-paying experience of established insurers.

Apartment Owner Insurance Coverage Checklist

Property Damage Coverage protects the building structure, including dwelling, additional structures, and landlord-owned contents. This coverage typically includes fire, wind, hail, theft, and vandalism on an all-risk or named-peril basis.

General Liability Coverage protects against third-party bodily injury and property damage claims. Common scenarios include slip-and-fall accidents, tenant injuries, and discrimination lawsuits. Most landlords carry at least $2 million in liability coverage.

Loss of Rental Income (also called Fair Rental Value) reimburses lost rent when tenants cannot occupy the property due to covered damage. This coverage includes additional living expenses and continues until the property is habitable again.

Equipment Breakdown Coverage protects against mechanical failures of HVAC systems, elevators, boilers, and electrical equipment. This coverage is particularly important for older buildings with aging mechanical systems.

Ordinance & Law Coverage pays additional costs to bring damaged buildings up to current building codes. This endorsement can be crucial for older properties where code requirements have changed since original construction.

Tenant-Caused Damage coverage protects against accidental damage caused by tenants beyond normal wear and tear. This includes situations like kitchen fires, water damage from overflowing bathtubs, or damage from moving furniture.

For comprehensive guidance on selecting appropriate coverage levels, consult with a qualified insurance professional who specializes in rental property protection.

Must-Have Apartment Owner Insurance Endorsements

Business Interruption Coverage extends beyond basic loss of rental income to cover additional expenses during repairs, including utilities, taxes, and loan payments. Extended indemnity periods of 180-365 days provide adequate recovery time.

Building Ordinance Coverage addresses the gap between actual cash value and replacement cost when building codes require upgrades. This endorsement covers the undamaged portion of buildings, demolition costs, and increased construction expenses.

Cyber Liability Protection becomes increasingly important as property management digitizes. Coverage includes data breach response, tenant notification costs, and liability for compromised personal information.

Assault & Battery Coverage protects against claims arising from violent acts on the property. This endorsement is particularly valuable for properties in higher-crime areas or with security personnel.

Crime Coverage protects against employee theft, tenant fraud, and money/securities losses. This coverage is essential for properties with on-site management or rent collection.

Boiler & Machinery Coverage extends equipment breakdown protection to include pressure vessels, air conditioning systems, and electrical equipment. This coverage often includes expediting expenses to minimize business interruption.

Pollution Liability Coverage addresses environmental contamination from heating oil spills, mold, or other pollutants. This coverage is crucial for older buildings with underground storage tanks or known environmental risks.

Vacancy Permit Coverage maintains protection when properties are temporarily unoccupied. Standard policies often exclude coverage after 30-60 days of vacancy, making this endorsement essential during tenant transitions.

Optional Add-Ons That Pay Off

Non-Payment of Rent Coverage reimburses unpaid rent and legal costs for eviction proceedings. This coverage typically includes attorney fees, court costs, and lost rent during the eviction process.

Tenant Discrimination Defense provides legal defense for fair housing claims and discrimination lawsuits. Coverage includes attorney fees, court costs, and damages up to policy limits.

Professional Liability Coverage protects property managers against errors and omissions claims. This coverage is essential for owners who actively manage properties or provide property management services.

Green Upgrade Coverage pays additional costs to rebuild with environmentally friendly materials and energy-efficient systems. This endorsement supports sustainability goals while potentially reducing future operating costs.

Resident Relocation Expenses covers costs to temporarily house displaced tenants during repairs. This coverage maintains tenant relationships and reduces vacancy losses during restoration.

FEMA research on disaster recovery shows that 25% of businesses don’t reopen after natural disasters, highlighting the importance of comprehensive coverage.

Cost, Discounts & Deductibles: What Drives Your Premium?

Apartment owner insurance premiums vary significantly based on property characteristics, location factors, and coverage selections. Understanding these variables helps owners optimize coverage while managing costs effectively.

Building Age significantly impacts premiums, with properties built before 1980 often facing higher rates due to outdated electrical, plumbing, and HVAC systems. Newer buildings with modern safety features typically qualify for preferred rates.

Number of Units affects both liability exposure and premium calculations. Single-unit properties may qualify for simplified coverage forms, while buildings with 7+ units require commercial apartment policies with higher liability limits.

Construction Type influences fire risk and premium rates. Frame construction costs more than masonry or fire-resistive buildings. Properties with sprinkler systems, fire alarms, and security systems often qualify for significant discounts.

Roof Condition directly impacts property coverage rates. Roofs over 20 years old may require inspections or updates for coverage eligibility. Some carriers offer credits for impact-resistant roofing materials.

Location Hazards including coastal exposure, earthquake zones, and high-crime areas affect premium calculations. Properties in FEMA flood zones require separate flood insurance, while coastal properties may need windstorm coverage.

Claims History influences renewal rates and coverage availability. Properties with frequent claims may face higher deductibles or coverage restrictions. Maintaining claim-free periods often qualifies for loss-free discounts.

Security Systems including monitored burglar alarms, surveillance cameras, and access control systems typically qualify for liability and theft discounts. Some carriers offer additional credits for smart home technology.

More info about apartment building insurance cost

| Property Type | Units | Annual Premium Range | Coverage Included |

|---|---|---|---|

| Studio Apartment | 1 | $1,200 – $1,800 | GL + Property + Loss of Rents |

| Small Building | 5 | $3,500 – $5,500 | GL + Property + BI + Equipment |

| Mid-Size Complex | 20 | $8,000 – $15,000 | Full Commercial Package |

What Does Apartment Owner Insurance Cost in 2024?

General Liability Coverage for apartment owners typically costs $67-$89 per month for standard $1 million/$2 million limits. This coverage protects against slip-and-fall claims, tenant injuries, and discrimination lawsuits.

Property Coverage rates average $0.16-$0.24 per $100 of total insured value, varying by construction type, age, and location. Business interruption coverage adds approximately 10-15% to property premiums.

Equipment Breakdown Coverage costs $200-$500 annually for typical apartment buildings, depending on the age and type of mechanical systems. This coverage often pays for itself with a single HVAC failure.

Earthquake and Flood Riders vary significantly by location and risk exposure. Earthquake coverage in Massachusetts costs substantially less than California, while flood insurance depends on FEMA zone designations.

In California, apartment owner insurance averages $1,341 annually or $112 monthly for small studio apartments, with costs increasing proportionally for larger properties and additional coverage features.

How to Save Without Cutting Coverage

Bundling Policies with the same carrier often provides 10-25% discounts on multiple coverage lines. Combining apartment insurance with personal auto, homeowners, or umbrella policies maximizes savings opportunities.

Monitored Security Systems including burglar alarms, fire detection, and surveillance cameras typically qualify for 5-15% liability discounts. Some carriers offer additional credits for smart home technology integration.

Sprinkler System Certification can reduce property premiums by 15-30% for eligible buildings. Annual inspections and maintenance records demonstrate system reliability to underwriters.

Higher Deductibles significantly reduce premiums while maintaining coverage limits. Increasing deductibles from $1,000 to $5,000 often saves 20-30% on property coverage costs.

Avoiding Small Claims helps maintain loss-free discounts and prevents premium increases. Handling minor repairs out-of-pocket preserves claims history for major losses.

Annual Policy Reviews ensure coverage remains appropriate as property values and rental income change. Regular reviews identify opportunities for coverage adjustments and premium optimization.

Learn more about lowering premiums

Claim Time: Navigating the Process Like a Pro

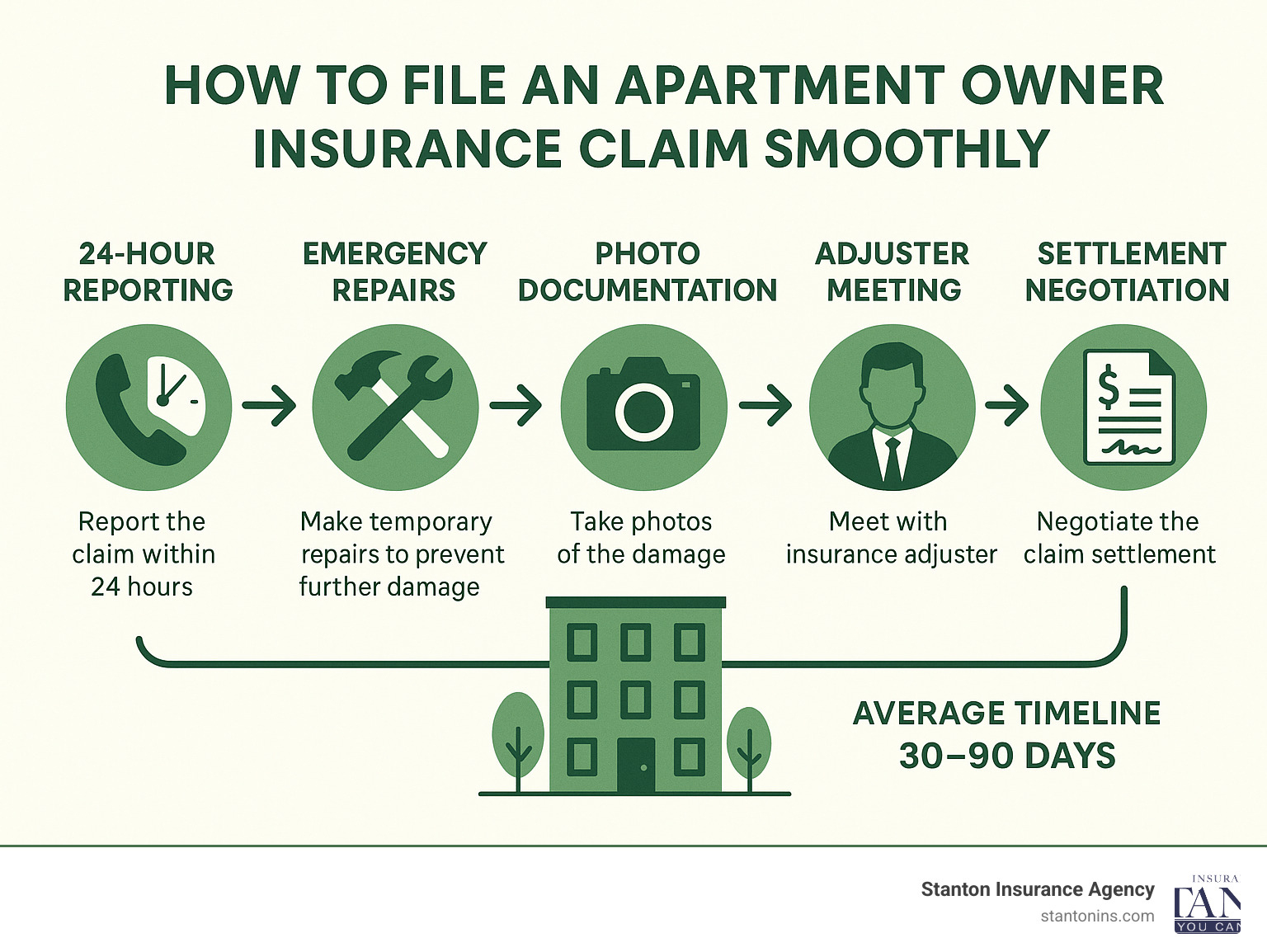

When disaster strikes your apartment property, quick action and proper documentation determine claim success. The first 24-48 hours after a loss are critical for preserving evidence, preventing additional damage, and initiating the claims process effectively.

Immediate Response begins with ensuring tenant safety and preventing further damage. Contact emergency services if needed, then notify your insurance carrier within 24 hours. Most carriers provide 24/7 claim reporting through phone hotlines or mobile apps.

Photo Documentation should capture damage from multiple angles before any cleanup begins. Include wide shots showing the overall scene and close-ups of specific damage. Date-stamp photos and maintain digital copies in cloud storage.

Tenant Communication requires balancing transparency with privacy concerns. Inform affected tenants about the claims process timeline while coordinating temporary housing if units become uninhabitable. Document all tenant-related expenses for potential reimbursement.

Emergency Repairs should be completed immediately to prevent additional damage, but document everything before starting work. Take photos, obtain written estimates, and save all receipts. Most policies cover reasonable emergency repair costs.

Adjuster Meetings provide opportunities to present your case effectively. Prepare a chronological timeline of events, gather all relevant documentation, and accompany the adjuster during property inspections. Point out all damage and explain any unique property features.

How to File an Apartment Owner Insurance Claim Smoothly

24-Hour Notice to your insurance carrier starts the claims process and establishes the loss date for coverage purposes. Have your policy number, property address, and basic loss details ready when calling.

Emergency Repairs should be completed immediately but documented thoroughly. Take photos before starting work, obtain written estimates from contractors, and save all receipts for potential reimbursement.

Claim Number Tracking helps organize all communications with your insurance company. Reference this number in all correspondence and keep detailed records of conversations with adjusters and claim representatives.

Loss of Rent Proof requires documentation of rental income and vacancy periods. Provide lease agreements, rent rolls, and vacancy records to support business interruption claims.

Code Upgrade Bids should be obtained from licensed contractors familiar with current building codes. These estimates support ordinance and law coverage claims for required upgrades during repairs.

Claim Diary maintenance helps track important dates, conversations, and decisions throughout the claims process. This documentation proves valuable if disputes arise or additional information is needed.

Common Apartment Owner Insurance Claim Pitfalls

Late Reporting can jeopardize claim coverage, especially for liability claims where early investigation is crucial. Most policies require “prompt” notification, typically within 24-48 hours of finding the loss.

Undocumented Upgrades may not be covered if not properly reported to your insurer. Maintain records of all property improvements and update your policy accordingly to ensure adequate coverage limits.

Under-Insured Values become apparent only during major losses when replacement costs exceed policy limits. Annual property appraisals help maintain adequate coverage as construction costs and property values increase.

Missing Ordinance Coverage can leave owners responsible for expensive code upgrades required during repairs. This endorsement is particularly important for older buildings where code requirements have changed significantly.

Ignoring Tenant Policies can complicate claims when tenant belongings are damaged. Encourage tenants to maintain renters insurance and understand the boundaries between landlord and tenant coverage responsibilities.

Frequently Asked Questions about Apartment Owner Insurance

Do I legally need apartment owner insurance?

Apartment owner insurance is not legally required by state law, but it’s highly recommended for financial protection. However, mortgage lenders typically require property insurance as a condition of financing, making coverage practically mandatory for financed properties.

Many property management companies and tenant lease agreements also require landlord insurance to protect against liability claims. Additionally, some municipalities require liability insurance for rental property licenses or permits.

While not legally mandated, the financial risks of operating uninsured rental properties are substantial. Liability claims, property damage, and lost rental income can quickly exceed an owner’s financial capacity without proper insurance protection.

What’s the difference between apartment owner insurance and tenant insurance?

Apartment owner insurance protects the property owner’s interests including building structure, liability exposure, and rental income. This coverage does not protect tenant belongings or tenant liability for damages they cause to others.

Tenant insurance (renters insurance) protects tenants’ personal property and provides liability coverage for damages tenants cause to others. This coverage is separate from and does not protect the landlord’s interests.

The key distinction is that landlord insurance covers the building and rental business risks, while tenant insurance covers personal belongings and tenant liability. Both types of coverage are important, but they serve different parties and purposes.

Landlords should require tenants to maintain renters insurance to protect tenant belongings and provide liability coverage for tenant-caused damages. This requirement reduces potential conflicts and ensures appropriate coverage for all parties.

How often should I review my apartment owner insurance policy?

Annual policy reviews are essential to ensure coverage remains adequate as property values, rental income, and risk exposures change. Schedule reviews at least 30 days before renewal to allow time for coverage adjustments.

Property Value Changes due to improvements, market appreciation, or depreciation should trigger coverage limit adjustments. Under-insurance can leave owners responsible for significant out-of-pocket costs during major losses.

Rental Income Fluctuations affect business interruption coverage needs. Increases in rental rates or occupancy levels may require higher loss of rental income limits to maintain adequate protection.

Risk Exposure Changes including new amenities, security systems, or tenant demographics may qualify for discounts or require coverage modifications. Regular reviews ensure policies reflect current property conditions.

Market Conditions and insurance company changes can create opportunities for better coverage or pricing. Annual reviews with your insurance agent help identify improvement opportunities and ensure competitive positioning.

Conclusion & Next Steps

Selecting the right apartment owner insurance provider requires careful evaluation of your property’s unique risks, coverage needs, and budget constraints. Our ranking system helps identify providers best suited for different property types and owner preferences.

National carriers excel for multi-state portfolios and comprehensive coverage packages, while specialty habitational underwriters provide expertise for challenging risks. Regional mutuals offer community focus and dividend potential, while independent agents provide choice and advocacy. Digital platforms emphasize convenience and efficiency for tech-savvy owners.

The key to success lies in matching provider strengths with your specific needs. Consider factors like property age, construction type, location risks, and coverage preferences when evaluating options. Don’t sacrifice essential coverage for premium savings, but do explore discounts and deductibles that optimize your cost-benefit ratio.

Regular policy reviews ensure coverage remains adequate as your property portfolio and risk exposures evolve. Annual discussions with your insurance professional help identify improvement opportunities and maintain competitive positioning in the marketplace.

At Stanton Insurance Agency, we understand the complexities of apartment owner insurance and work with multiple carriers to provide customized solutions for Massachusetts, New Hampshire, and Maine property owners. Our commercial insurance expertise and local market knowledge help apartment owners steer coverage decisions with confidence.

More info about apartment building insurance quote

Ready to protect your apartment investment? Contact us today for a comprehensive review of your insurance needs and competitive quotes from top-rated carriers. Your rental property deserves the protection that comes from working with experienced professionals who understand the apartment insurance market.